CSRD

Coperate Sustainability Reporting Directive

CSRD solution: Get ready to report

Get a complete overview of the EU directive with an implementation and governance framework that helps you implement and structure your CSRD efforts.

Break down the complexity

With the EU directive on sustainability reporting, companies face challenges that will fundamentally impact their compliance work. However, implementing a regulatory framework without understanding its scope and relying on Excel to structure the process can be intimidating and overwhelming.

With RISMA, you can structure the CSRD process, develop policies and procedures, define roles and responsibilities, and consolidate information and data.

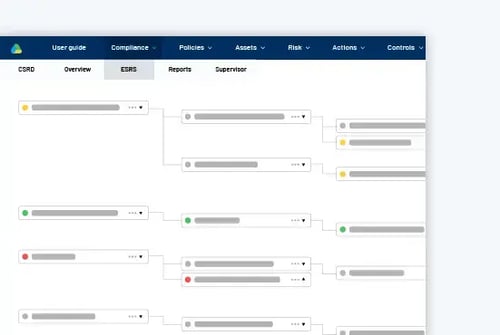

Understand the scope of the ESRS

Gain insight and a complete overview of the 12 European Sustainability Reporting Standards (ESRS) in one source.

Pre-loaded with all the disclosure requirements and 1.144 data points, the solution is broken down into individual E-S-G nodes to ease navigation. It provides you with the correct information when needed.

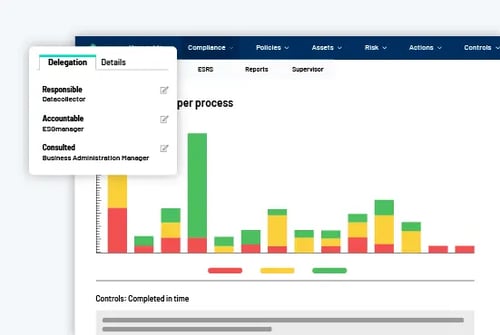

Empower and engage your organization

It is easy to lose track of complex projects. Keep everyone on the same page and empower people to make decisions about what and when by delegating roles and responsibilities.

Share knowledge and learn fast. Because ESG compliance is not just about action plans and controls - it's about empowering and engaging the entire organization.

Start where you are

Your ESG efforts have been worthwhile. Most of your previous work on sustainability – GRI, SASB, UN GLOBAL COMPACT- human rights due diligence, climate or materiality assessment, and others are part of the documentation requirements in the CSRD reporting.

Add all your policies and control data and create your new CSRD baseline.

Stop shuffling around Excel spreadsheets and emails

Bring your ESG efforts to the next level

CSRD reporting starts with a compliance framework

You may be on the lookout for a CSRD reporting tool. But to collect and document the extensive amount of qualitative and quantitative information, both forward-looking and retrospective, you will need a project framework that prepares your organisation for compliant reporting.

With RISMAs CSRD solution, you will get a project framework tailored explicitly for the CSRD reporting work. Compliance and completeness are no longer limited to Legal and Finance teams.

What topics do you need to report on?

Apply double materiality

Transition plans for climate change aligned with 1,5 degree scenario

Transition plans biodiversity aligned with no-net-loss scenario

Actions and action plans for all disclosure requirements

Documentation of governance framework

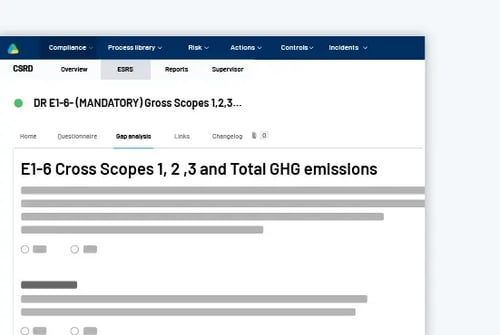

Scope 1, 2 and 3 emissions

Risk Management

And much more

Building blocks of the CSRD solution

Learn how we can structure your CSRD efforts

We help more than +500 organizations succeed with their governance, risk and compliance, and we would love to help you too.

A GRC platform to bring the organization together

Power your organisation by connecting data, teams, action and reporting in an integrated GRC platform. Whether you deploy one, two, or all our solutions, RISMA GRC platform provides great value by boosting collaboration, increasing visibility, and saving time for everyone involved.

-

Internal audit streamlined

-

Effortlessly automate, document and report all your controls - including assessment, mitigation and monitoring in one simple platform.

-

Risk management organized

-

Define, assess, analyze and mitigate your organization’s risks and turn your insight into strategic assets.

-

ESG made efficient

-

Set clear goals, track processes and document progress, ensuring the sustainability strategy is turned into action and reality.

FAQ

How do I know whether my company is subject to report on the CSRD regulations?

To begin with, the CSRD will include approx. — 49,000 companies across EU member states. Starting from January 1st, 2024, companies with over 500 employees, including those already reporting on the Non-Financial Reporting Directive (NFRD), will be the first required companies to report on their sustainability performance under the Corporate Sustainability Reporting Directive (CSRD). This will primarily be listed companies, insurance companies, and banks. Initially, CSRD will include approx. 49,000 companies across EU member states.

However, to get a comprehensive understanding of whether your company is subject to report on the CSRD regulations, it is recommended that you reach out to your company advisors. They have the expertise to provide tailored advice based on crucial factors such as:

- The size of your company

- Its legal entity status

- Its revenue

What should I report on in my CSRD report?

The CSRD reporting should comply with the EU's reporting standards, ESRS, which include environmental, social, and corporate governance (ESG) aspects

e.g.

Environment

- Climate change

- Water resources

- Circular economy

- Pollution

- Biodiversity

Social

- Equal opportunities for all

- Working conditions

- Respect for human rights

Governance

- Management's responsibilities regarding the company's sustainability

- Corporate Ethics and Culture

- Company control and risk management in relation to sustainability risks

However, we recommend you contact your company advisor or consultant to determine if your company should report and what your company specifically needs to report on according to your CSRD report.

How do I report on CSRD?

Please contact your company advisor or auditor if your company meets the mandatory reporting requirements under CSRD. All final reports must support digital tagging and are to be published as part of the public financial reporting.

RISMA's CSRD solution can be part of your company's tech stack to make this task more manageable. We set a project framework to prepare you and your company for CSRD reporting.